Can I Buy a Car Before Closing on a House?

You found the house. You made the offer. The bank approved your mortgage. Now you're in escrow — that 30-to-45-day waiting period before the deal officially closes and you get the keys.

Everything feels done. So when you spot a great deal on a new car, it's tempting to think: why not?

Here's why not: buying a car during escrow is one of the fastest ways to lose your mortgage approval. And it happens to buyers every single year.

Will Buying a Car Affect My Mortgage Approval?

The simple answer is, yes. When you applied for your mortgage, the bank looked at your financial picture at that moment: your income, your credit score, and your debt-to-income ratio (DTI). They approved you based on those numbers.

The problem is, your mortgage approval isn't final until the day you close. And lenders don't just trust that nothing has changed since your application. They check again.

Most mortgage lenders are required to re-verify your finances immediately before closing , often just 1 to 3 days before your closing date. A new car loan shows up instantly.

A car loan does three things to your mortgage application at once:

It raises your debt-to-income ratio. A $500/month car payment added to your existing debts can push your DTI above the lender's maximum — even if you were comfortably within limits before.

It temporarily lowers your credit score. Every new loan application triggers a hard inquiry on your credit report. That can knock your score down at the worst possible moment.

It reduces your cash reserves. Lenders want to see that you have money left after your down payment and closing costs. A down payment on a car eats into those reserves.

What Is Debt-to-Income Ratio and Why Does It Matter?

Your debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments. If you earn $7,000 a month and your total debt payments are $2,800, your DTI is 40%.

Most conventional lenders cap debt-to-income at 43–45%. FHA loans allow up to 50-55% in some cases. You were approved because your DTI was within those limits, but add a car payment… and you might not be anymore.

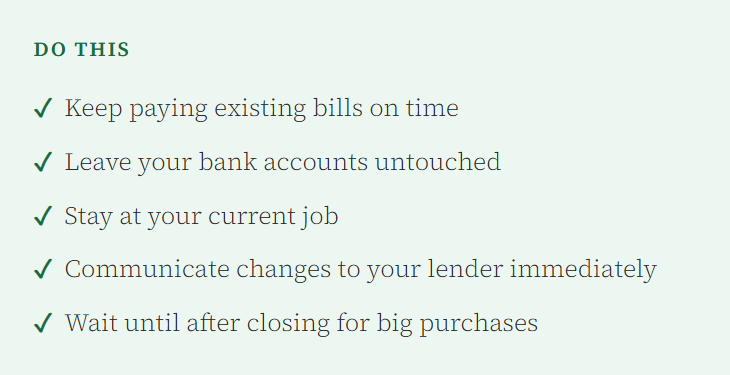

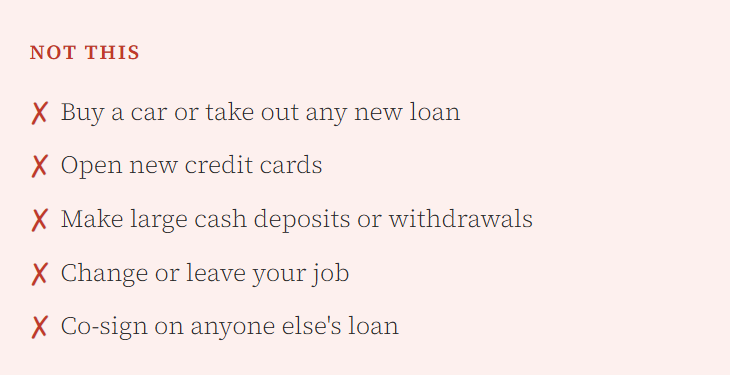

What Not to Do During Escrow

A car is a drastic example, but it's not the only trap. Here's what to avoid from the moment your offer is accepted until after your closing date:

When Can I Buy a Car After Closing on a House?

The safest answer: the day after you close. Once the deed is recorded and the mortgage is fully funded, your home purchase is complete. Your lender can no longer touch your approval.

Here's a bonus: some financial advisors note that your credit score is actually in strong shape immediately after closing on a mortgage. You've just demonstrated the ability to secure and qualify for a large loan. Car lenders often respond well to this.

Wait until after you have the keys. Then go get the car.

Need Guidance?

If you are thinking about buying a home and need strategic guidance, I’m Amy, a real estate agent serving Whatcom County Washington. Give me a call or text to get started! I’m happy to help. 360-296-6904